JOB WORK & ITC UNDER GST

Job work Means: –

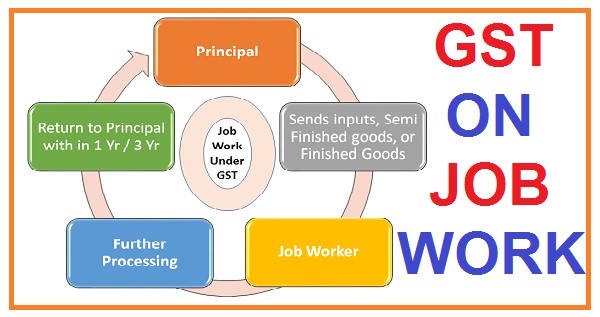

As per GST Act “job work” means any treatment or process undertaken by a person on goods belonging to another registered person.

The person who does the said job work called ‘job worker’.

Accordingly;

Job work means any treatment or processing undertaken by a person (i.e. Job Worker) on raw materials or semi-finished goods which is supplied by the principal manufacturer.

ITC on Job work: –

The registered person (i.e. principal manufacturer) will be allowed to take input tax credit (ITC) of GST paid on purchase of goods.

There is no restriction if certain condition is fulfilled to take the credit of tax paid on the purchase of goods sent to job work.

Condition are to be fulfilled in relation to ITC: –

- Capital goods/Input can be sent to the job-worker without payment of tax:-

- From Principal place of business.

- Directly from the place of supply of the supplier of such goods.

- Effective date for Capital goods/Input sent depends on place of business:

- If goods send from the principal’s manufacturer place of business- Date of goods sent out.

- If goods send directly from the place of supply of the supplier of such goods to the job worker- Date of receipt of the goods by job worker

- Capital goods/Input are required to be returned back by principal manufacturer: –

- Capital Goods: – 3 Years from the date of sending of such goods to the job worker.

- Input: – 1 Years from the date of sending of such goods to the job worker.

- In case Capital goods/Input are not returned back within the period 3 year or 1 year respectively, such Capital goods/Input will be treated as supply from the effective date mentioned above and GST will be payable by the principal manufacturer.

Document required to be maintained to take ITC under GST: –

The responsibility of the principal manufacturer is to maintain proper records or documents for the inputs or capital goods which is sent to the job worker.

If principal manufacturer wants to claim ITC on goods send to job worker from principal place of business or directly sent to the job worker from the place supplier of the goods, then it required to issue challan for goods. Challan must include the following information:

- Name, address and GSTIN of principal manufacturer

- Job worker information

- Date and number of the delivery challan

- HSN code, description and quantity of goods

- Taxable value, tax rate, tax amount- CGST, SGST, IGST, UTGST separately

- Place of supply and signature

Note:

- The details of delivery challans issued to the job worker must be shown in FORM GSTR-1.

- Details of delivery challans issued to the job worker must also be filed through Form GST ITC – 04.