Amnesty Scheme to GSTR-9 non-filers

TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

(DEPARTMENT OF REVENUE)

CENTRAL BOARD OF INDIRECT TAXES AND CUSTOMS

NOTIFICATION

NO. 07/2023–CENTRAL TAX

New Delhi, dated the 31st March, 2023

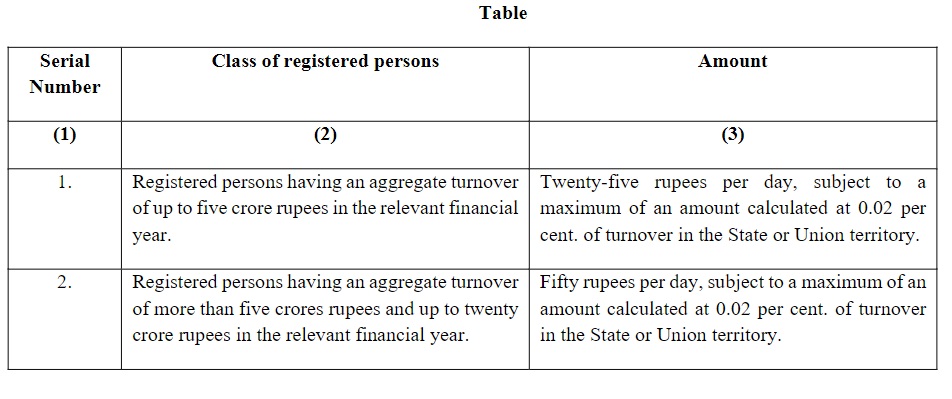

S.O…… (E). In exercise of the powers conferred by section 128 of the Central Goods and Services Tax Act, 2017 (12 of 2017)(herein after referred to as the said Act), the Central Government, on the recommendations of the Council, hereby waives the amount of late fee referred to in section 47 of the said Act in respect of the return to be furnished under section 44 of the said Act for the financial year 2022-23 onwards, which is in excess of amount as specified in Column (3) of the Table below, for the classes of registered persons mentioned in the corresponding entry in Column(2) of the Table below, who fails to furnish the return by the due date, namely:-

Provided that for the registered persons who fail to furnish the return under section 44 of the said Act by the due date for any of the financial years 2017-18, 2018-19, 2019-20, 2020-21 or 2021-22, but furnish the said return between the period from the 1stday of April, 2023 to the 30thday of June, 2023, the total amount of late fee under section 47 of the said Act payable in respect of the said return, shall stand waived which is in excess of ten thousand rupees.

[F.No.CBIC-20013/1/2023-GST]

(Alok Kumar)

Director