Budget 2023: Key Points For Taxpayers & Which Income Tax Regime is better

The Union budget 2023 presented in the Parliament today on 1st February 2023, the Finance Minister proposed five major announcements for tax payers:

1. Nil tax, upto income Rs. 7 Lakhs (After Rebate U/S 87A)

2. Six Income slabs and new tax rates

3. Standard Deduction Rs. 52,500/- for salaried person with an income of Rs. 15.5 Lakhs or above.

4. Surcharge on Income above 2 Cr 25% instead of 37%

5. Encashment of earned leave upto 10 months of average salary, at the time of retirement in case of an employee (other than an employee of the Central Government or State Government), is exempt under sub-clause (ii) of clause (10AA) of section 10 of the Income-tax Act to the extent notified. The maximum amount which can be exempted is Rs. 3 Lakhs at present. It is proposed to issue notification to extend this limit to Rs. 25 Lakhs

Note: ALL THE ABOVE CHANGES (Sr. 1 TO Sr.4 )IS APPLICABLE ONLY IN NEW INCOME TAX REGIME, NO CHANGES IN OLD INCOME TAX REGIME. It means you can get benefit of above changes if you select new tax regime. Nil tax in old tax regime, Upto income Rs. 5 Lakhs (After Rebate U/S 87A). No change in Income tax slab and rate in old tax regime. No changes in Standard Deduction for salaried person with an income of Rs. 15.5 lakhs of above if you selecting old tax regime. No change in surcharge is proposed for those who opt to be under the old regime.

Some more important changes:

- Standard deduction of Rs.50,000/- to salaried individual, and deduction from family pension up to Rs.15,000/- is currently allowed only under the old regime. It is proposed to allow these two deductions under the new regime also.

- Tax on capital gains can be avoided by investing proceeds of such gains in residential property. This is proposed to be capped at Rs.10 Cr.

- The income from market linked debentures is proposed to be taxed as short-term capital gains at the applicable rates.

- New income tax regime as the default tax regime. However, citizens will continue to have the option to avail the benefit of the old tax regime.

New Tax Regime as an alternative to the existing Old Tax Regime for Individual and HUFs. Since the Old Tax Regime is optional by all means, a taxpayer now has a choice to make between the New and Old Tax Regime after a careful comparison supported by facts and figures.

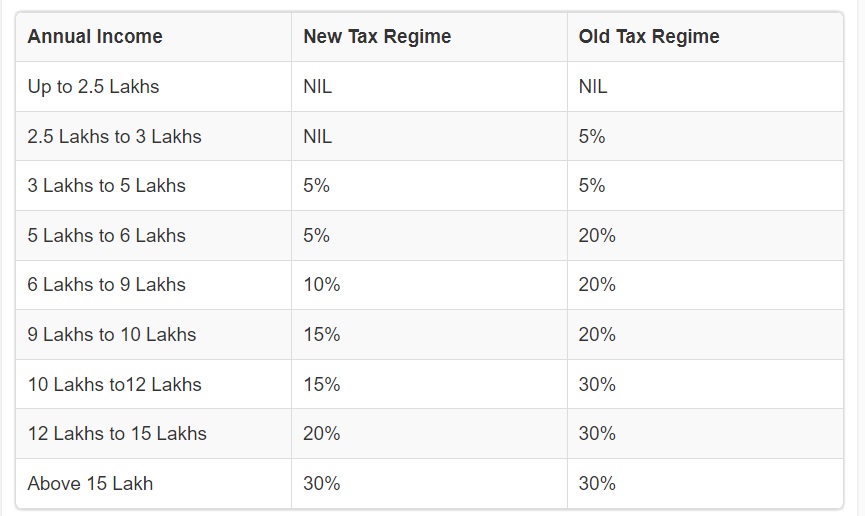

Income Tax rates under the new tax regime and the old tax regime:

In above table it is clearly showing that the new tax regime has proposed lower income-tax rates, for income segments up to Rs 15 lakh, but you need to remember that the proposed lower tax rates will be applicable only if you are willing to give up exemptions and deductions available under various provisions of the Income-tax Act, 1961. This means that when you choose the New Tax Regime, you will have to forgo some exemptions and deductions available under chapter VI A of the Act that grant deductions under Section 80. Even the deduction on home loan interest, under Section 24(b) will be disallowed. Around 70 exemptions and deductions have been removed in the New Tax Regime.

Some of the 70 exemptions and deductions you won’t get in new regime:

- Leave travel allowance Section 10(5)

- House rent allowance Section 10(13A)

- Children Education Allowance

- Housing loan interest

- Section 80C investments

- Medical insurance premium U/S 80D

- Expenses actually paid for medical treatment of specified diseases and ailments U/S 80DDB

- Education loan interest U/S 80E

- Rent paid for furnished/unfurnished residential accommodation U/S 80GG

- Deduction in respect of donations to certain funds, charitable institutions U/S 80G

- Interest on deposits in saving account U/S 80TTA Interest on deposits U/S 80TTB for senior citizens

- Deduction for a certified person with a disability by the medical authority U/S 80U

Will taxpayer gain by switching to new regime?

The Ministry of Finance expects four out of five Income taxpayers to move to the new tax regime. It has analysed the income and investment data of 57.8 million taxpayers and found that 69% would prefer to save on tax under the new system. Another 20% might want to switch to avoid the hassles and paperwork involved in tax planning.

Taxpayer who avail several exemptions and deductions such as house rent allowance and Section 80C deductions may not benefit from switching to the new system. Taxpayer will be able to make the choice depending on their financial situation and depending on what is best suitable from a tax planning point of view. The budget has tried to put more money in the hands of taxpayers by curtailing the incentives to save. Section 80C forces individuals to save, and they will be weaned off savings if there is no tax incentive. The impetus seems to be towards spending, rather than focusing on longer term financial security for taxpayer. Taxpayer who opt for the new tax regime and forgo tax exemptions may end up spending money rather than use it towards their financial safety and security.