Export of services under GST

The Government is always concerned about the country’s exports and therefore, they are pretty keen to pamper the exporter by incentivizing and providing certain privileges to them. On the other hand, it is the utmost duty of the government’s department to curb down the fraudster who pretend to be the exporter and defrauding the revenue by their illicit activities. Below are the provisions in GST related to export of service.

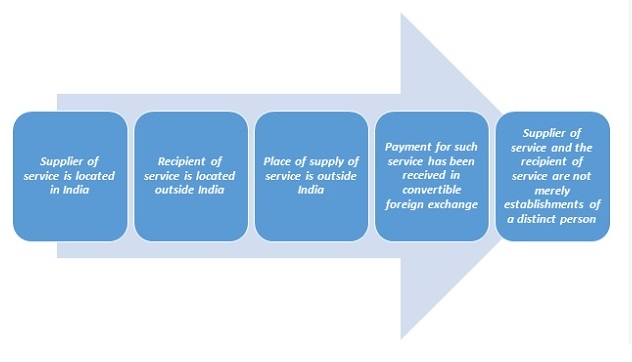

As per section 2(6) of IGST Act, 2017, “export of services” means the supply of any service when, ––

(i) the supplier of service is located in India;

(ii) the recipient of service is located outside India;

(iii) the place of supply of service is outside India;

(iv) the payment for such service has been received by the supplier of service in convertible foreign exchange or in Indian rupees wherever permitted by the Reserve Bank of India; and

(v) the supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with explanation 1 in section 8;”

Explanation 1 in section 8 of the Act provides that where a person has an establishment in the taxable territory and any other establishment in a non-taxable territory or having establishments in one or more taxable territory in India shall be treated as establishments of distinct persons.

So there are five limbs for determination of export of service and we will analyze one by one as follows

Service provider is located in taxable territory:

Location of the supplier is defined under Clause 71 of Section 2 of CGST Act, 2017 which provides that the location of supplier will be,

- The registered place of business of service provider

- If the supply is made from other than the place of business, that other location

- If supply is made from more than one establishments, the location of the establishment most directly concerned with the provisions of the supply

- In absence of any such place, the location of the usual place of residence of the supplier

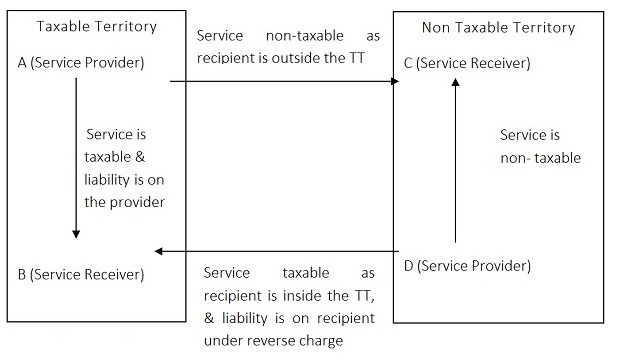

Therefore, the service provider shall be located and registered in India.

Recipient is outside India:

Location of the service recipient is defined under Clause 70 of Section 2 of CGST Act, 2017 which is in line with Clause 71 as mentioned above. The location of service recipient will be,

- The registered place of business of service recipient

- If the supply is received at a place other than place of business, that other location

- If supply is received at more than one establishments, the location of the establishment most directly concerned with the receipt of the supply

- In absence of any such place, the location of the usual place of residence of the recipient

So, to be eligible for export benefit under GST, the service recipient must be located outside India i.e. the recipient shall not be registered in India under GST whether directly or indirectly.

Place of supply of services is outside India:

With regard to compliance with this clause which states that for services to qualify as export, place of supply of service must be outside India, reliance has to be placed on Section 13 of IGST Act, 2017. As per section 13, place of supply shall be as follows,

| Sr No. | Service Description | Example | Place of Supply |

|---|---|---|---|

| 1 | Services provided in respect of goods which are required to be available to supplier for performing such services including services provided by electronic mean but excluding repair of goods which are temporarily imported into India and exported without put to use in India | Upgradation of Computer | – Where services are performed – In case services performed by electronic mean i.e. online, where the goods are situated |

| 2 | Services provided to an individual representing either as the recipient or on the behalf of recipient, which require the physical presence of such individual | Make-over service provided to a Model or Actor, Health checkup services | Where services are actually performed |

| 3 | Services provided directly in relation to an immovable property including expert and estate agent services, accommodation by Hotel, Inn etc., grant of right to use immovable property for construction work including architects and decorator services | Architect services, Interior Decorator, Rental Services, Construction Contracts | Where the Immovable property or Hotel, Inn etc. is located |

| 4 | Services provided by way of admission to a cultural, artistic, sporting or any other entertainment events or amusement park and services ancillary to it | Admission to IPL match (ticket) | Where the event is actually held or the location of the park |

| 5 | Services provided by banks, other financial institution | Bank charges etc. | Location of supplier of Service |

| 6 | Intermediary Services | Agent Services | Location of supplier of Service |

| 7 | Services consisting of hiring of means of transport, including yachts but excluding aircrafts and vessels, up to a period of one month | Hiring Taxi | Location of supplier of Service |

| 8 | Service of transportation of goods other than by way of mail or courier | Hiring vessel for import of goods/GTA services | Location of destination of such goods |

| 9 | Passenger Transportation Services | Bus Service/Airlines Services | The place passenger embarks on the conveyance for continuous journey |

| 10 | Services provided on board a conveyance | The first scheduled point of departure of such conveyance | |

| 11 | Online Information and Database access or retrieval services | Google, LinkedIn | Location of Service Recipient |

There is a residual subsection, subsection 2 which provides that the place of supply of service shall be the location of service receiver except the services as specified above.

Therefore, to sum up, for determining the place of supply of a service, firstly it is to be seen whether the service falls under any of the specific situations as mentioned above, the place of supply shall be considered accordingly. In all other cases, resort has to be made to residual subsection which provides that the place of supply of service shall be the location of service receiver.

So, the place of supply shall be seen in light of the provisions of Section 13 of IGST Act, 2017 which has to be outside India to qualify for the export and export benefits.

Payment of services is received in convertible foreign exchange or in INR wherever permitted by RBI:

This is the most important limb for the determination of transaction to be eligible for export. Payment shall be received in Foreign Currency. The receipt in foreign currency will ultimately fulfil the real objective of export.

The supplier of service and the recipient of service are not merely establishments of a distinct person:

Explanation I in section 8(2) of the IGST Act, 2017 states that where a person has an establishment in India and any other establishment outside India then such establishment shall be treated as establishment of distinct persons.

So, if the service provider and receiver are establishments of distinct person, then it will not be covered under export and thus not eligible for export benefits.

Now, question may arise that whether Holding company and its subsidiaries are establishments of distinct person. On this issue, Gujarat High Court has given a laudable judgment in the case of Linde Engineering India Pvt. Ltd. & Ors. Vs. Union of India. The court held that the rendering of services by a subsidiary company in India to its parent Company located in Germany which is a company separately registered in non-taxable territory (Germany) cannot be considered as services provide to merely establishment of distinct persons.

Therefore, Holding-Subsidiary relation does not tantamount establishment of distinct person.

However, where the Indian arm is set up as a liaison office or a branch they would be treated as establishments of the same entity and hence the supply inter se shall not qualify as export of services.