Form and manner of furnishing of return

Rule 61 of CGST Rule : Form and manner of furnishing of return-

(1) Every registered person other than a person referred to in section 14 of the Integrated Goods and Services Tax Act, 2017 (13 of 2017) or an Input Service Distributor or a non-resident taxable person or a person paying tax under section 10 or section 51 or, as the case may be, under section 52 shall furnish a return in FORM GSTR-3B, electronically through the common portal either directly or through a Facilitation Centre notified by the Commissioner, as specified under –

(i) sub-section (1) of section 39, for each month, or part thereof, on or before the twentieth day of the month succeeding such month:

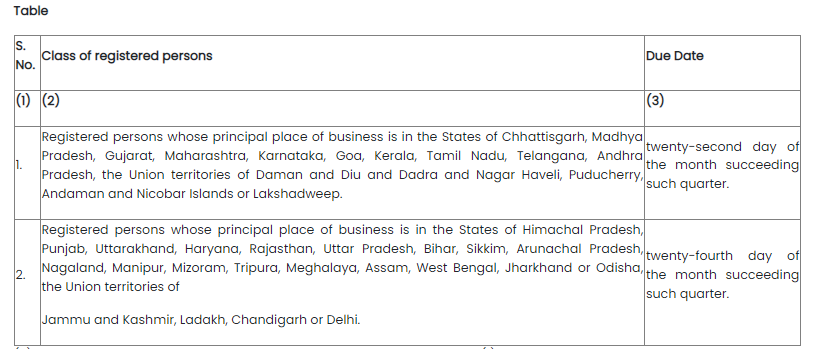

(ii) proviso to sub-section (1) of section 39,for each quarter, or part thereof, for the class of registered persons mentioned in column (2) of the Table given below, on or before the date mentioned in the corresponding entry in column (3) of the said Table, namely:-

(2) Every registered person required to furnish return, under sub-rule (1) shall, subject to the provisions of section 49, discharge his liability towards tax, interest, penalty, fees or any other amount payable under the Act or the provisions of this Chapter by debiting the electronic cash ledger or electronic credit ledger and include the details in the return in FORM GSTR-3B.

(3) Every registered person required to furnish return, every quarter, under clause (ii) of sub rule (1) shall pay the tax due under proviso to sub-section (7) of section 39, for each of the first two months of the quarter, by depositing the said amount in FORM GST PMT-06, by the twenty fifth day of the month succeeding such month:

Provided that the Commissioner may, on the recommendations of the Council, by notification, extend the due date for depositing the said amount in FORM GST PMT-06, for such class of taxable persons as may be specified therein:

Provided further that any extension of time limit notified by the Commissioner of State tax or Union territory tax shall be deemed to be notified by the Commissioner:

Provided also that while making a deposit in FORM GST PMT-06, such a registered person may –

(a) for the first month of the quarter, take into account the balance in the electronic cash ledger.

(b) for the second month of the quarter, take into account the balance in the electronic cash ledger excluding the tax due for the first month.

(4) The amount deposited by the registered persons under sub-rule (3) above, shall be debited while filing the return for the said quarter in FORM GSTR-3B, and any claim of refund of such amount lying in balance in the electronic cash ledger, if any, out of the amount so deposited shall be permitted only after the return in FORM GSTR-3B for the said quarter has been filed.