Furnishing of evidence by employee for TDS deduction on Salary for FY 2021-22

IMPORTANT CIRCULAR

No. AN/PAY- 1/1447/I-TAX/2021-2022

0/0 THE C.D.A., RIDGE ROAD, JABALPUR- 482001

DATE: – 15.09.2021

To,

The Officer-in-Charge

All sections o Main Office

All S Offices

Subject:- Furnishing of evidence of claims by employee for deduction of tax under section 192 for the FY 2021-22 and AY 2022-23. (For Assessees other than those who opted for New Tax Regime)

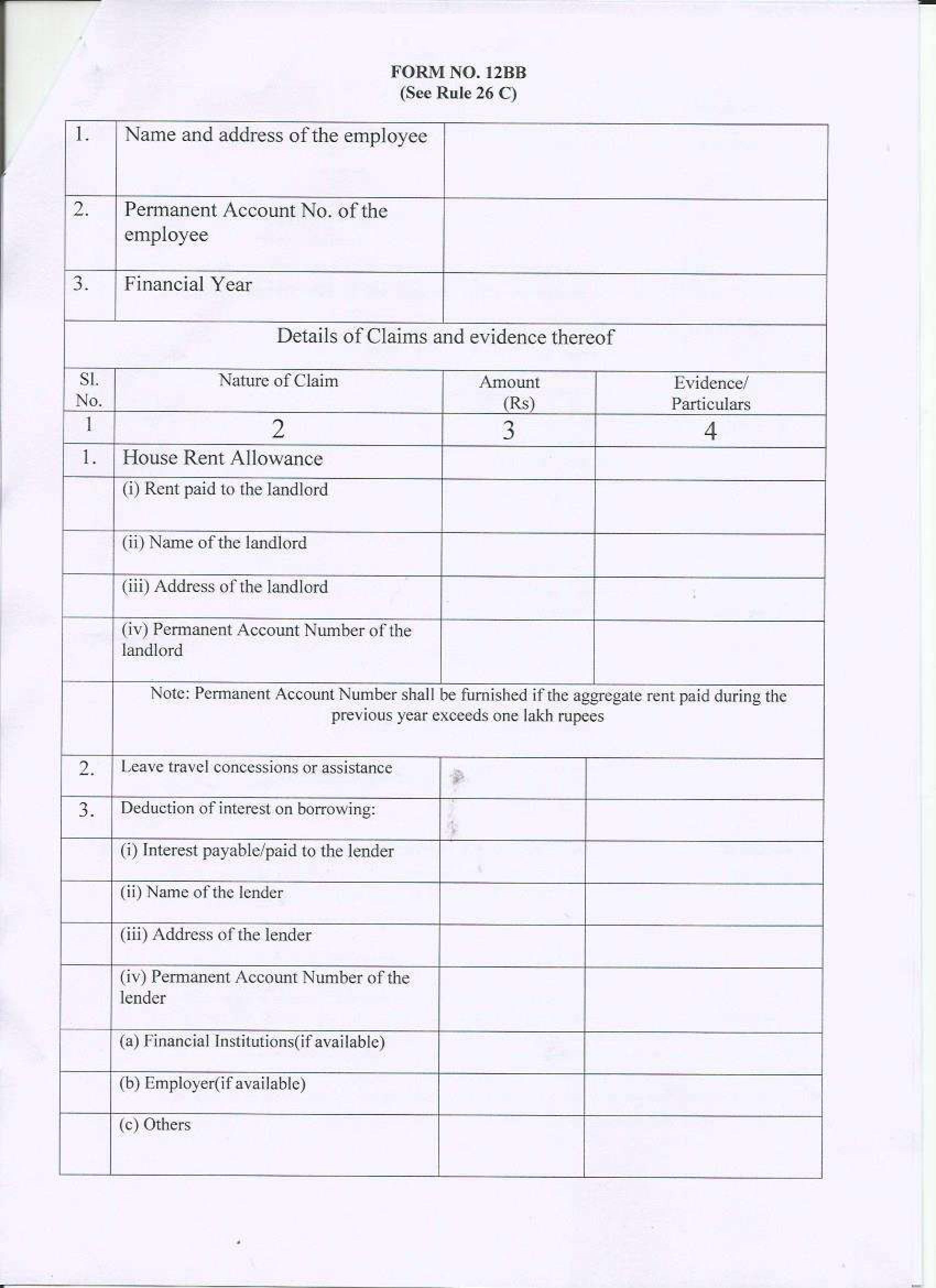

According to Rule 26 (C) of Income Tax Rules, the assessee shall furnish to the person responsible for making payment under sub-section (1) of section 192, the evidence or the particulars of the claims referred to in sub-rule (2), in Form No. 12BB (specimen enclosed) for the purpose of estimating his income or computing the tax deduction at source.

(2) The assessee shall furnish the evidence or the particulars .specified in column 0. of the Table below. of the claim specified in the corresponding entry in column (2) of the said

Table:—

| S. No. | Nature of claims | Evidence or particulars |

|---|---|---|

| (1) | (2) | (3) |

| 1. | House Rent Allowance | Name, address and permanent account number of the landlord/landlords where the aggregate rent paid during the previous year exceeds rupees one lakh |

| 2. | Leave travel concession or assistance or assistance. | Evidence of expenditure |

| 3. | Deduction of interest under the head “Income from house property”. | Name, address and permanent account number of the lender. |

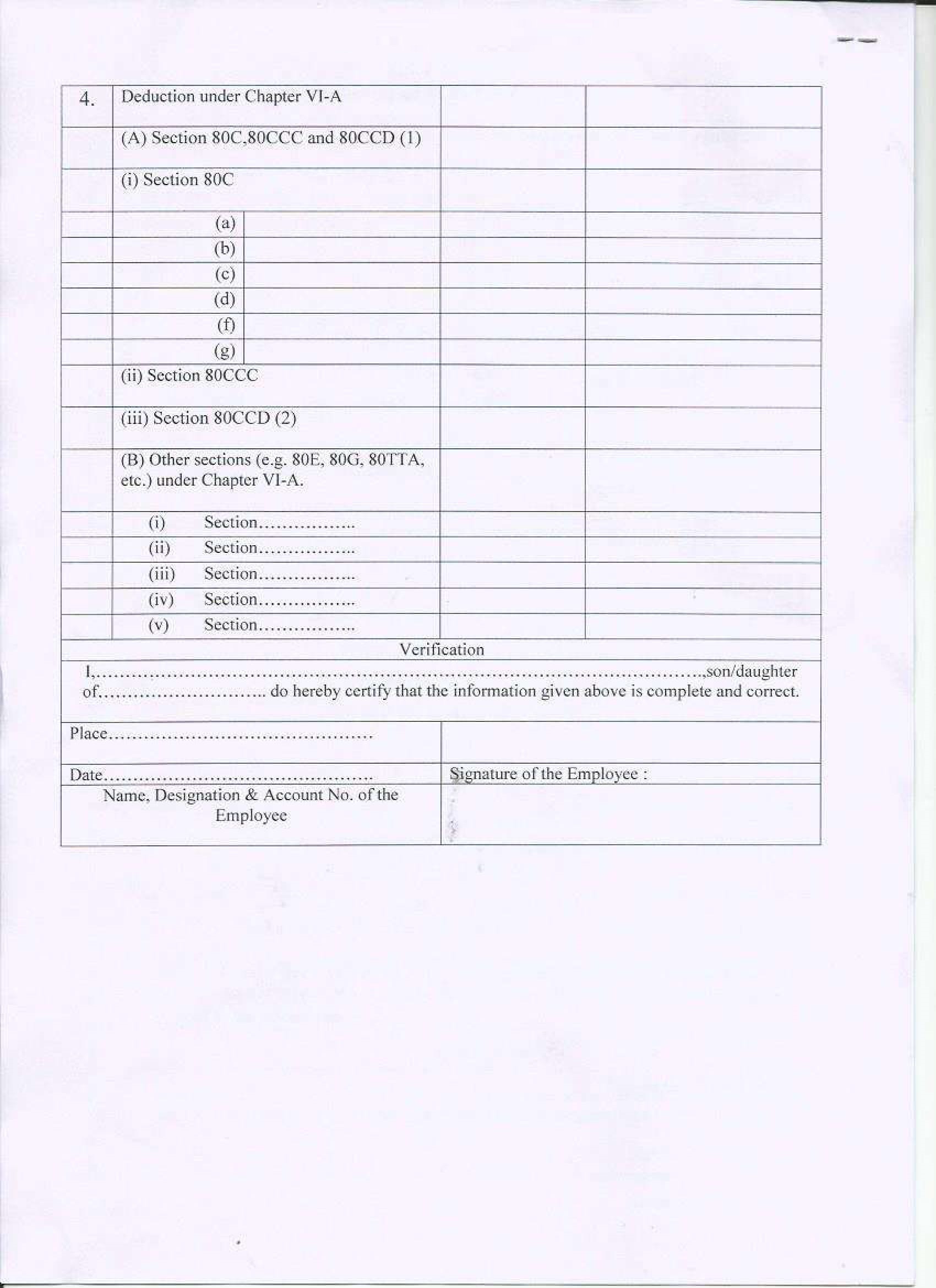

| 4. | Deduction under Chapter VI-A | Evidence of investment or expenditure |

Note 1: Assessees claiming relief under section 89 through Form-10 E will submit all supporting documents Viz. Form-16 and/or copy of ITR-V (Acknowledgement) of all years mentioned in Form-10 E, due-drawn statement of arrears received duly indicating arrear amount of each year (year = March to February) along with their Form-1286.

Before submitting evidence for the financial year 2020-21 the following points may be ensured:-

1. Information regarding Income under any other head:

(i) Section 192(2B) enables a taxpayer to furnish particulars of income under any head other than “Salaries” ( not being a loss under any such head other than the loss under the head ” Income from house property”) received by the taxpayer for the same financial year and of any tax deducted at source thereon. The particulars may now be furnished in a simple statement which is properly signed and verified by the taxpayer in the manner as prescribed under Rule 2613(2) of the Rules and shall be annexed to the simple statement. The form of verification is reproduced as under:

Computation of income under the head “Income from house property”.

While taking into account the loss from House Property, the employee must files the declaration referred to above and encloses therewith a computation of such loss from house property in a separate statement (copy enclosed). Details shall be submitted in respect of loss claimed under the head “Income from house property” separately for each house property:

Please also ensure furnishing of the evidence or particulars in Form No. 12BB in respect of deduction of interest as specified in Rule 26C read with section 192(2D).

2. Conditions for Claiming Deduction of Interest on Borrowed Capital for Computation of Income from House Property [Section 24(b)]:

Section 24(b) of the Act allows deduction from income from houses property on interest on borrowed capital as under:-

(i) the deduction is allowed only in case of house property which is owned and is in the occupation of the employee for his own residence. However, if it is actually not occupied by the employee in view of his place of the employment being at other place, his residence in that other place should not be in a building belonging to him.

(ii) The quantum of deduction allowed as per table below:

| SI No | Purpose of borrowing capital | Date of borrowing capital | Maximum Deduction allowable |

|---|---|---|---|

| 1 | Repair or renewal or reconstruction of the house | Any time | Rs. 30,000/- |

| 2 | Acquisition or construction of the house | Before 01.04.1999 | Rs. 30,000/- |

| 3 | Acquisition or construction of the house | On or after 01.04.1999 | Rs. 1,50,000/- (upto AY 2014- 5) Rs. 2,00,000/- (w. e. f. AY 2015-16) |

In case of Serial No. 3 above

(a) The acquisition or construction of the house should be completed within 3 years from the end of the Pi’ in which the capital was borrowed. Hence, it is necessary for the DDO to have the completion certificate of the house property against which deduction is claimed either from the builder or through self-declaration from the employee.

(b) Further any prior period interest for the FYs upto the FY in which the property was acquired or constructed (as reduced by any part of interest allowed as deduction under any other section of the Act) shall be deducted in equal installments for the FY in question and subsequent four FYs.

(c) The employee has to furnish before the DDO a certificate from the person/institution i.e. lender to whom any interest is payable on the borrowed capital specifying the amount of interest payable. In case a new loan is taken to repay the earlier loan, then the certificate should also show the details of Principal and Interest of the loan so repaid.

Note: Employees seeking exemption of HBA interest (under section 24 b – income from house property) as well as principal are required to submit certificate from bank authorities (lender) duly indicating the interest to be paid and principal actually paid in the current Financial year with the date of issue of loan and loan amount and also their PAN. Employees are also advised to submit a simple statement of computation of loss from house property (Format enclosed).

Meaning of Self-occupied property A self-occupied property means a property which is owned/ occupied throughout the year by the owner for the purpose of his own residence and is not actually let out during the whole or any part of the year. Thus, a property not occupied by the owner for his residence cannot be treated as a self occupied property. However, there is one exception to this rule. If the following conditions are satisfied, then the property can be treated as self-occupied and the annual value of a property will be “Nil”, even though the property is not occupied by the owner throughout the year for his residence:

a) The taxpayer owns a property;

b) Such property cannot actually be occupied by him owing to his employment, business or profession carried on at any other place and he has to reside at that other place in a building not owned to him:

c) The property mentioned in (a) above (or part thereof) is not actually let out at any time during the year;

d) No other benefit is derived from such property.

3. Employees seeking exemption on account of self disability/dependant are required to submit attested valid copies of disability certificate issued by Medical Board as well as an undertaking showing statement of expenditure incurred, otherwise exemption will not be allowed.

4. Quoting of correct PAN is compulsory on all documents.

The contents of this circular may please be brought to the notice of all officers and staff members for strict compliance. The required information/statement alongwith supporting documents may be sent to this office by 15th October, 2021 positively. If claim is not received, duly supported with evidence, within the stipulated time, recovery of Income Tax will be made automatically in portion as per calculation done by the System and Income Tax once deducted will not be refundable by this office.

Please acknowledge receipt.

End:- As stated above

-Sd-

(Rupesh Kumar Singh)

Accounts Officer

Copy to:-

The Officer I/c

OA Cell (local) : For uploading on official website.

STATEMENT ON INCOME FROM HOUSE PROPERTY

In respect of —- ————-(PAN- )

| 1 | Address of House Property | ||

|---|---|---|---|

| Is the Property Co-owned (Pi. Tick) | Yes | No | |

| If Yes, percentage of share | |||

| Please Tick, if Self-occupied or let out/deemed let out | Self-occupied Yes / No | Let out/deemed let out Yes / No |

|

| a | Annual lettable value or rent received or receivable | ||

| b | The amount of rent which cannot be realized | ||

| c | Tax paid to local authorities | ||

| d | Total (lb+1c) | ||

| e | Annual value (1a-ld) (nil if self-occupied as per Section 23(2) of the Act) | ||

| f | Annual value of the property owned (own percentage share x 1e) | ||

| g | Standard deduction (30% of 1f) | ||

| h | Interest payable on borrowed capital (Maximum limit as per Section 24b of the Act) | ||

| i | Total (1g+1h) | ||

| j | Income from House Property (1f-1i) | ||

| 2 | Date of borrowing the loan and purpose | ||

| 3 | Whether the property has been acquired/constructed within 5 years of from the end of FY in which capital was borrowed. if yes, specify the FY of acquisition/ construction completion. | ||

| 4 | (i) Certificate of interest payable from lender attached | Yes | |

| (ii) Evidence of share percentage in the property (Pl. Tick) |

NOTE: 1. This statement may be submitted in respect of each house property for which deduction under section 24 and/or loss adjustment under section 71 of I.T. Act has been claimed in the assessment.

DECLARATION

Note: 2. I, ……………………………………… (name of the assessee), do declare that what is stated above is true to the best of my information and belief.

Signature :

Name :

Designation/Account No.:

FORM NO. 12BB

(See Rule 26 C)