Leave Encashment Income Tax Treatment

What is Leave encashment?

Leave encashment is an equivalent amount received by an employee for the unutilized leaves during a tenure. Calculation of leave encashment is based on salary of the employee. The benefit of leave encashment may be provided by employer to employee during employment, at the time of termination of employment or at the time of retirement of employee.

Tax Treatment of Leave encashment

The tax treatment of leave encashment depends on when is it availed by the employee, during employment, at retirement or termination otherwise and the nature of employer, central or state government or non government.

Leave encashment tax treatment can be summarized as following:

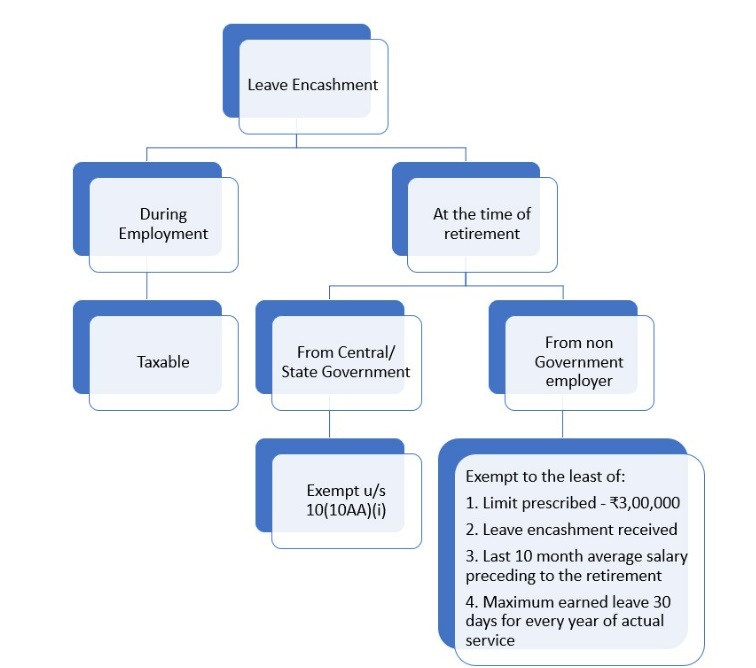

1. Received during the course of employment – Where leave encashment is received during the employment then the same shall be taxed in the hands of employee under the head Salary. However the benefit of Section 89 can be availed by filing Form 10E.

2. Received at the time of retirement from Central or State Government – Leave encashment received from Central or State Government is exempt from tax u/s 10(10AA)(ii).

3. Received at the time of retirement from employer other than Central or State Government – Leave encashment received from employer other than Central or State Government is exempt to extent lowest of the following as per section 10(10AA)(ii):

4. Limit specified by Central Government by notification in Official Gazette, specify in this behalf having regard to the limit applicable in this behalf to employee of that Government, currently the same is ₹3,00,000

5. Payment for the period of earned leave at his credit at the time of retirement whether on superannuation, calculated on basis of 10 month average salary and where earned leave does not exceed 30 days for each year of service.

6. Actual leave encashment received [Please refer chart for easy understanding]

Let us understand this with the help of some examples:

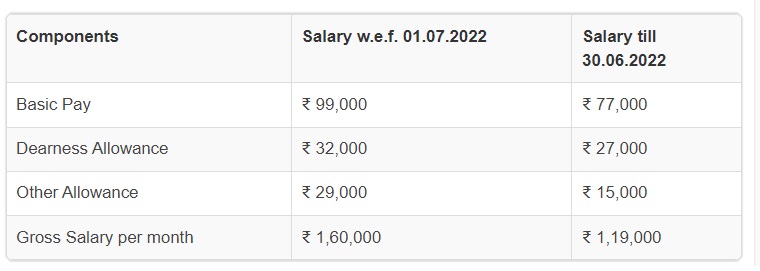

Mr. Navankur is retiring from private software company after 32 years of service on 31.12.2022 and gets 35 leaves per annum. His salary got revised w.e.f. 01.07.2022. His per month salary components are as follows:

He has utilized 320 leaves till retirement, leaving balance of 800 leaves. He receives Leave encashment of ₹ 42,67,000 at the time of retirement.

Let us see how much exemption he can get u/s 10(10AA)(ii)

As per Section 10(10AA)(ii), least of the following will be exempt in hands of Mr. Navankur

i. ₹3,00,000 as notified by the government

ii. Last 10 months Average salary – For 10 month average salary we shall consider salary of last 10 months which would be from March till December 2022 coming out to be ₹ 12,02,000 Note: here Salary means Basic pay, DA and commission received by employee as fixed percentage of turnover.

iii. Leave encashment calculated considering 30 day leaves per year maximum for every completed year of service – ((32 years x 30 leaves*) – 320 utilized leaves) x ₹ 4367per day salary = ₹ 34,93,333

iv. Actual leave encashment – ₹ 42,67,000

The least of above is ₹3,00,000. Thus Exempt amount shall be ₹3,00,000 (assuming that he has never claimed leave encashment exemption u/s 10(10AA)(ii)) out of total received amount of ₹ 42,67,000 and balance ₹ 39,67,000 shall be taxable under the head salary.

*Please Note that in condition 3 of above example we have considered maximum annual leaves of 30 only as per Explanation to Section 10(10AA)(ii). For purpose of this condition, not more than 30 leaves per year can be considered to be provided by employer.

Now a logical thought arising in the minds of reader would be that can we claim this exemption every time we get leave encashment at the time of resignation/ termination from employer. The answer is yes, you may claim this exemption however the total exemption available to a person in lifetime is ₹3,00,000. Thus if a person changes employer and has received leave encashment from non-government employer then, the limit of ₹ 3,00,000 would be reduced by leave encashment exemption claimed by employee earlier in previous tax returns. If in above example Mr. Navankur has changed employer in FY 2016-17 and had claimed exemption of ₹ 1,40,000 then he can claim only ₹1,60,000 (balance out of ₹ 3,00,000) at the time of retirement, i.e., for FY 2022-23.

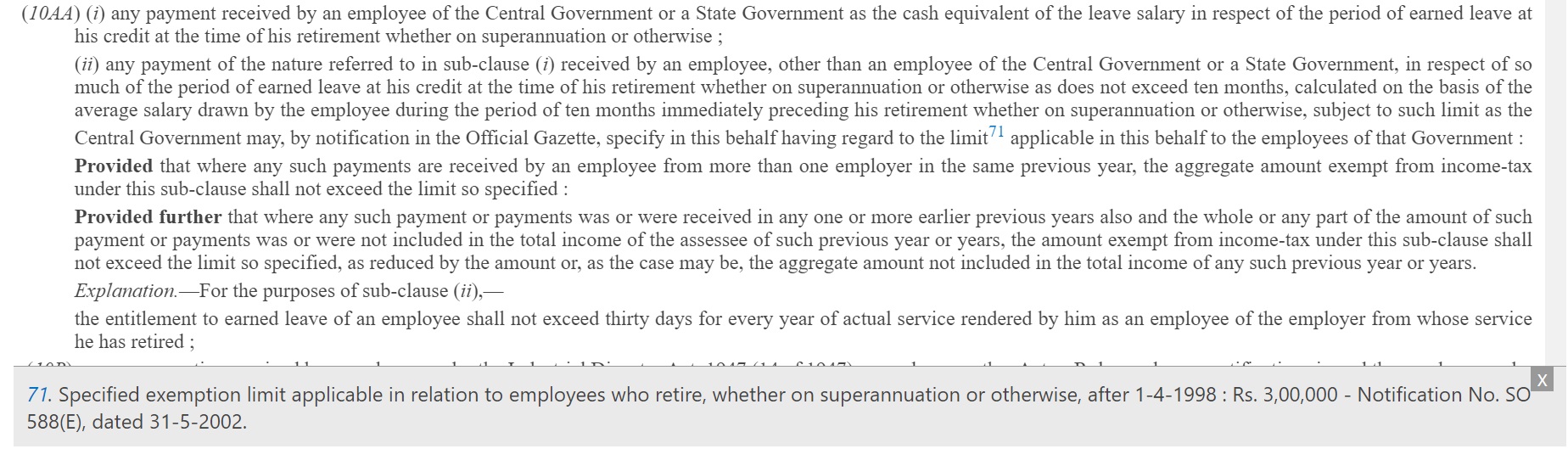

Another point worth noticing about leave encashment Section 10(10AA)(ii) is that the maximum threshold exemption of ₹3,00,000 is limit decided by the government from time to time and notified in official gazette. The benchmark for deciding this limit is leave encashment received by a government employee, Gazette is just a medium for notifying the amount of leave encashment available to government employee. Thus, Gazette is not determining the threshold limit but just notifying the threshold limit which is already decided. In bare act one may read Section 10(10AA)(ii) says that “subject to such limit as the Central Government may, by notification in the Official Gazette, specify in this behalf having regard to the limit71 applicable in this behalf to the employees of that Government” [please refer snip attached]. That means CBDT has to notify the amount of leave encashment available to the government employee which unfortunately has been last notified on 31.05.2002 in gazette notification no. SO 588E. The intention of lawmaker here is to provide exemption to the non government employee equivalent to what exemption is available to government employee in respect to leave encashment but the intention has not been met as no official notification is released by CBDT in this respect.

As per the data available in public domain the leave encashment of government employee receiving highest salary (Cabinet Secretary) is ₹29.25 lakhs. Thus the limit of ₹ 3,00,000 should be updated for the spirit of law. However until the same is notified by CBDT in Official Gazette ₹3,00,000 should be followed as threshold limit.

Frequently Asked Questions on Taxability of Leave encashment

1. Can anyone claim Leave encashment exemption irrespective of residential status?

Yes, as per Section 10(10AA) the exemption is available to anyone whose income is subject to tax in India

2. Can I claim leave encashment for all the leaves annual leave, sick leave, sabbatical leave, maternity leave etc.

The act does not create any difference in the types of leaves. Employer policy however may be refereed for the same purpose. For calculating leave encashment, employer policy would prevail and for calculation of income tax exemption for leave encashment income type of leave is not relevant.

3. If leave encashment is received by heirs of deceased then what are the tax implications?

In such a case leave encashment is fully exempt in the hands of legal heirs.

Extract of Section 10(10AA) of Income Tax Act, 1961