New Tax Rate For A.Y. 2021-22

New section 115BAC has been introduced in the Act which has provided an option to Individual/HUF to opt for the new tax regime which has following key points: –

-

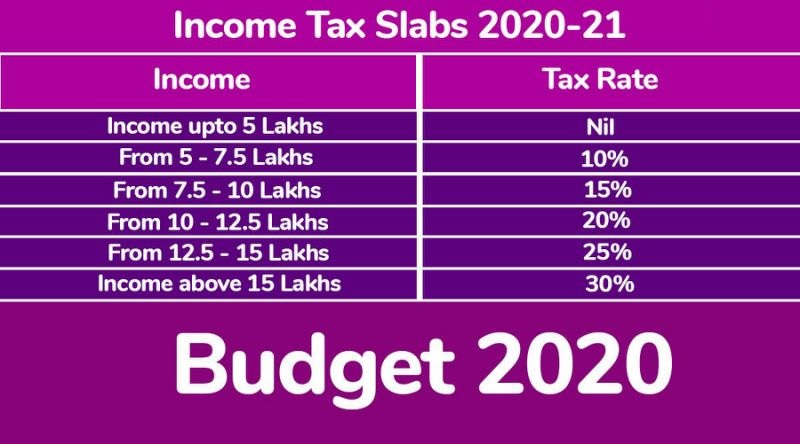

New Rate of Income Tax:-

S. No. Total Income Rate of Tax 1 Upto Rs. 2,50,000 Nil 2 From Rs. 2,50,001 to Rs. 5,00,000 5 per cent 3 From Rs. 5,00,001 to Rs. 7,50,000 10 per cent 4 From Rs. 7,50,001 to Rs. 10,00,000 15 per cent 5 From Rs. 10,00,001 to Rs. 12,50,000 20 per cent 6 From Rs. 12,50,001 to Rs. 15,00,000 25 per cent 7 Above Rs. 15,00,000 30 per cent - The new section 115BAC is applicable to Individual and HUF (Hindu Undivided Family) only.

- The new section 115BAC is optional. An assessee may opt or may not opt for the same in any assessment year.

- Cess @ 4% is leviable on the amount of income tax and surcharge, if any.

- Rebate under Section 87A continues for a resident individual whose total income does not exceed 5,00,000. The amount of rebate is 100% of income tax calculated before cess or 12,500 whichever is less.

-

If the new scheme is adopted the following deductions shall not be available to the assessee:-

- LTC (Leave Travel Concession) u/s 10(5), HRA (House Rent Allowance), section 10(13A), deduction under section 10(14), section 10(17), section 10(32), section 10AA, section 16.

- Deduction u/s 24(b) except u/s 24(a) under Income from house property

- Additional depreciation u/s 32(1)(iia)

- Deduction u/s 32AD, 33AB, 33ABA, 35, 35AD, 35CCC

- Chapter VIA deduction except deduction under section 80CCD(2) & section 80JJAA

- Brought forward losses and unabsorbed depreciation etc

- For detailed deduction and losses which is not allowable in the new tax regime please click link below

https://www.indiabudget.gov.in/doc/Finance_Bill.pdf