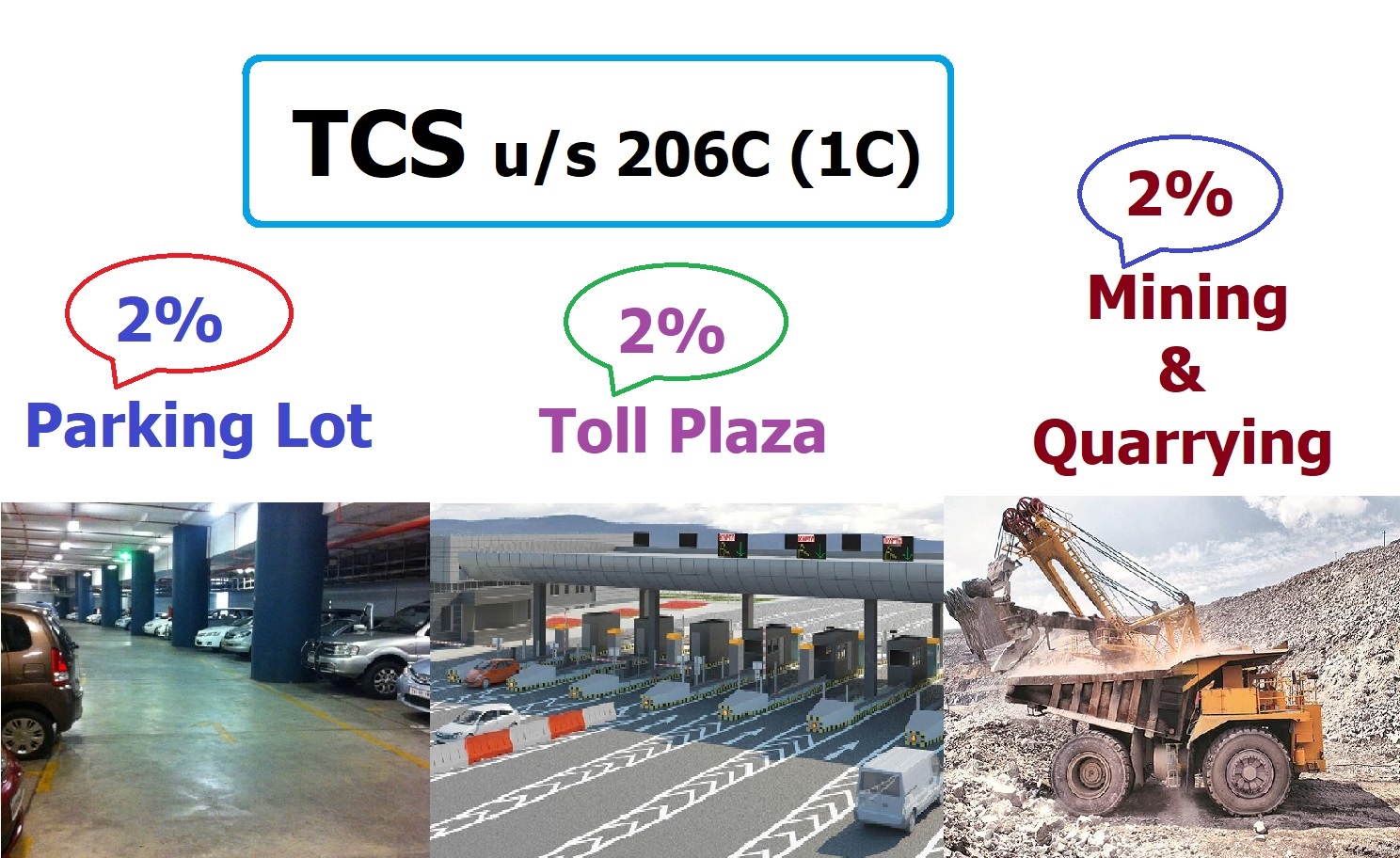

TCS in case of Parking lot, Toll plaza, Mining and quarrying

Every person, who grants a lease or a licence or enters into a contract or otherwise transfers any right or interest either in whole or in part in any parking lot or toll plaza or mine or quarry, to another person, other than a public sector company (hereafter in this section referred to as “licensee or lessee”) for the use of such parking lot or toll plaza or mine or quarry for the purpose of business shall, at the time of debiting of the amount payable by the licensee or lessee to the account of the licensee or lessee or at the time of receipt of such amount from the licensee or lessee in cash or by the issue of a cheque or draft or by any other mode, whichever is earlier, collect from the licensee or lessee of any such licence, contract or lease of the nature specified in the Table below, a sum equal to the percentage, specified in the corresponding entry in the said Table, of such amount as income-tax.

Summary of Section 206C (1C) of the Income Tax Act

- Threshold Limit: Any amount

- Rate of TCS:

| S. No. | Nature of Goods | Rate |

| (i) | Parking lot | 2% |

| (ii) | Toll plaza | 2% |

| (iii) | Mining and quarrying | 2% |

- Point to be Noted:

- “Mining and quarrying” shall not include mining and quarrying of mineral oil.

- “Mineral oil” includes petroleum and natural gas.

- TCS is not required to collect if the licensee or lessee is a public sector company.

- Higher Rate of TCS

As per section 206CC if PAN is not furnished by the collectee then TCS shall be collected at the higher of the following rates, namely: —

-

- at twice the rate specified in the relevant provision of this Act; or

- at the rate of 5%

- Time of collection:

Collector/Seller is required to collect TCS within earlier of the following dates:

-

- At the time of debiting of the amount payable by the buyer to the account of the buyer or

- At the time of receipt of such amount from the said buyer in cash or by the issue of a cheque or draft or by any other mode