TDS on Cash Withdrawal: Section 194N

As per section 194N, all the Banks to which Banking Regulation Act applies including a Co-operative Society and a post office shall be responsible to deduct TDS, if any person withdraws cash from the account/s maintained with them, being the amount or aggregate of amounts exceeding rupees one crore during the financial year.

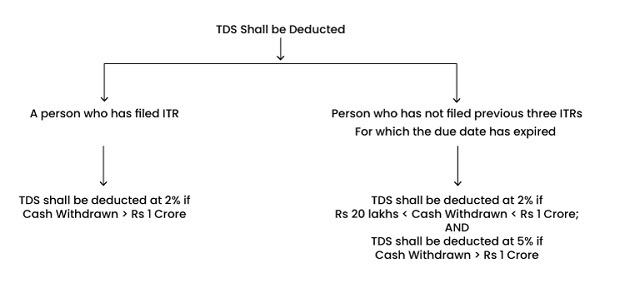

So, if any person withdraws cash in a financial year more than rupees one crore from one or more account/s maintained with a bank, a co-operative society, or a post office, such person shall be subject to TDS of 2% by such bank, co-operative society or a post office. If PAN not available then TDS shall be deducted at the rate of 20%.

This section was amended w.e.f 1st July 2020, that, if any person withdrawing cash, has not filed the ITRs for immediately three preceding financial years and the date to file these returns under section 139(1) has expired, then TDS rate and cash withdrawal limit changes. In such cases, TDS shall be deducted at the rate of 2% if the cash withdrawal is more than rupees twenty lakhs and up to rupees one crore. If such a person withdraws cash more than rupees one crore in the financial year, the TDS shall be deducted at the rate of 5%. In these cases, too, if the PAN is not available, the TDS rate shall be 20%.

Section 194N is not applicable: If cash withdrawal by the following then Banks, co-operative society or post office shall not require to deduct TDS:-

- The Government;

- Any banking company or a co-operative society which is engaged in the business of carrying on the business of banking or a post office;

- Business correspondent of a banking company or a co-operative society engaged in the business of carrying on the business of banking in accordance with the guidelines issued by RBI in this regard;

- Any White Label Automated Teller Machine (WLATM) of a banking company or a co-operative society engaged in the business of banking;

- Any such persons as may be notified by the Central Government subject to fulfillment of the conditions.

Point to be Noted:

- TDS shall be deducted at the basic rate (i.e., 2% or 5%) and surcharge or education cess shall not be applicable.

- Provisions of Section 197, where the tax is either not to be deducted or to be deducted at a lower rate shall not apply to this section.

- Any person, who, in the previous years has not filed the return of income on account of not having income chargeable to tax, such person shall be considered as a non-ITR filer for this section.