TDS on Rent Section 194I

Summary of section 194-I of Income Tax Act: –

- Deductor/ Payer: – Any person (Including Individual/HUF if they are liable to audit u/s 44AB)

- Deductee/ Payee: – Resident person

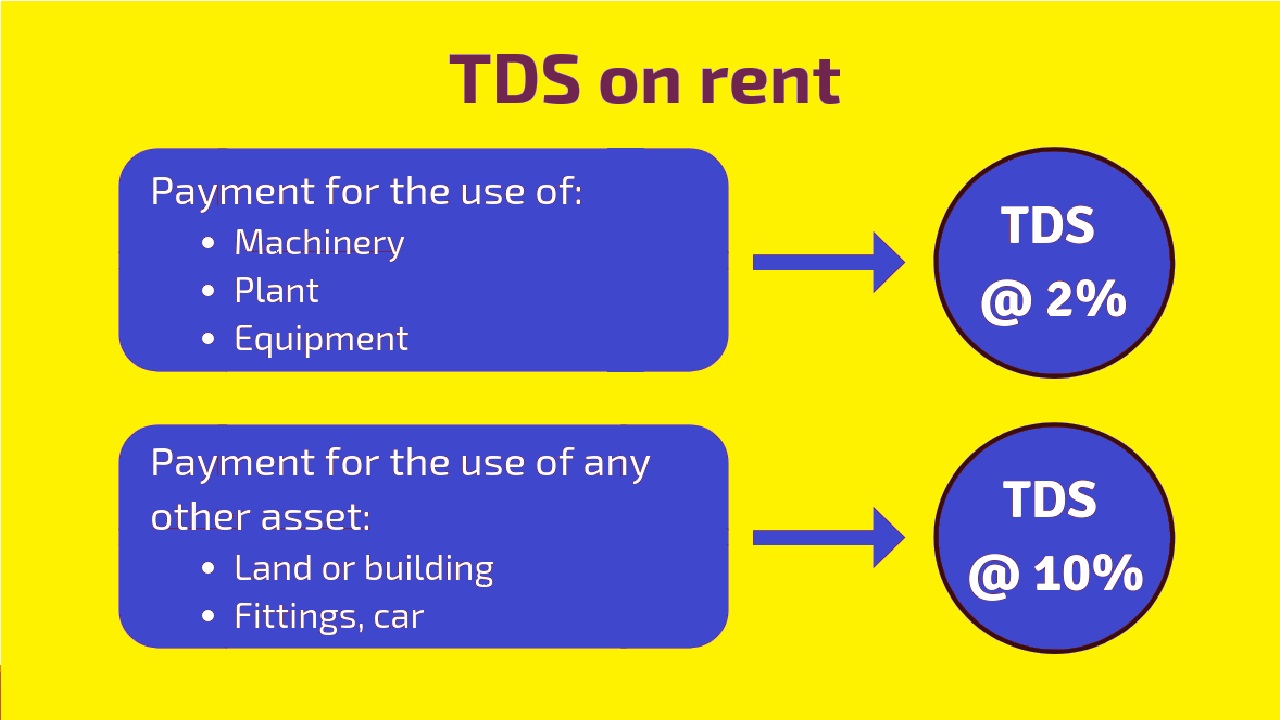

- Rate of TDS: –

- Use of any machinery or plant or equipment: – 2%.

- Use of any land or building (including factory building) or land appurtenant to a building (including factory building) or furniture or fittings: – 10%

- Threshold Limit

- Aggregate of the amount credited or paid or likely to be credited or paid during the financial year exceed Rs. 240000/-.

- Time of deduction: –

- At the time of credit of such income to the account of the payee or at the time of payment thereof in cash or by the issue of a cheque or draft or by any other mode, whichever is earlier.

- No TDS: –

- No TDS is required to be deducted if aggregate of the amount credited or paid or likely to be credited or paid during the financial year equal to or less than Rs. 240000/-.

- If payer or deductor is Individual/HUF and they are not labile to audit u/s 44AB.

- No deduction of TDS under this section where the income by way of rent is credited or paid to a business trust, being a real estate investment trust, in respect of any real estate asset, referred to in clause (23FCA) of section 10, owned directly by such business trust.

- Higher Rate of TDS: –

- TDS must be deducted @ 20% on the transaction amount if PAN is not provided by the payee.

Explanation. —For the purposes of this section, —

- “rent” means any payment, by whatever name called, under any lease, sub-lease, tenancy or any other agreement or arrangement for the use of (either separately or together) any, —

-

- land; or

- building (including factory building); or

- land appurtenant to a building (including factory building); or

- machinery; or

- plant; or

- equipment; or

- furniture; or

- fittings,

-

- where any income is credited to any account, whether called “Suspense account” or by any other name, in the books of account of the person liable to pay such income, such crediting shall be deemed to be credit of such income to the account of the payee and the provisions of this section shall apply accordingly.