UCO Bank invites online application for engagement as Concurrent Auditors

Application For Engagement Of Concurrent Auditor With UCO Bank (2021-2022) [For The Period 01-10-2021 TO 30-09-2022]- Last date for submission of application is 18-09-2021.

UCO BANK

AUDIT & INSPECTION DEPARTMENT

HEAD OFFICE, KOLKATA

NOTIFICATION

Date : 12.09.2021

[EXPRESSION OF INTEREST FOR ENGAGEMENT OF CONCURRENT AUDITORS]

Online application portal will remain open from

13.09.2021 to 18.09.2021 (23:59:59 hrs)

UCO Bank invites online application from practicing firms of Chartered Accountants in India for engagement as Concurrent Auditors to undertake Concurrent Audit assignment in designated branches/ offices through computerized application package and RLHs/AMBs/Service branches, Central Pension Processing Centre, SME Hubs, Treasury, Depository services and HO departments in India through manual process.

The firms who are willing to undertake the audit in computerised application environment have to apply for Concurrent Audit through online application portal.

I. ELIGIBILITY CRITERIA FOR ENGAGEMENT:

CA Firms not under cooling period ( i.e. no continuous audit for last three consecutive years in any branches /offices of UCO Bank) are eligible for applying as per list of branches mentioned in Annexure – I. For CA firms already engaged with us and not under cooling and their branch is listed in Annexure – II (Branches which are not identified for 2021-22) may apply for branches listed in Annexure – I.

a) CA firm should preferably be a partnership concern having experience in the field. The Bank may also consider the sole proprietorship concerns and in that case they would be also required to submit a declaration that they are full time practicing Chartered Accountants, not employed elsewhere, do not have any other business interest with UCO Bank and not a Director in UCO Bank or related to any of the present Directors of UCO Bank.

b) Applicant should either be a LLP / Partnership firm or Proprietorship, already in the panel of the RBI, which are circulated among the Banks for Statutory Branch Audit of the Banks from time to time. Registration with RBI and category allotted by RBI are mandatory.

c) The Concurrent Audit firm should furnish the name, qualification and skill set of the persons, who shall be conducting audit in the branch, to the Bank before commencing audit assignment and such persons will have to continue audit for all the Twelve (12) months.

d) The Concurrent Audit firm shall not lobby directly or indirectly for considering any credit proposals of their friends / clients to the Bank / auditee branch.

e) The Auditors’ Services should not have been terminated or stopped by our bank earlier for (i) want of satisfactory performance or (ii) serious acts of commission or omission or (iii) professional misconduct or (iv)any other adverse reasons.

f) If the name of the ECA is appearing in the list of Third Party Entities- TPEs prepared by IBA, or list of entities blacklisted by professional bodies such as ICAI or blacklist of other banks, then no empanelment would be considered.

g) The eligible auditor / LLP / Firm should have their office / infrastructure in the proposed Centre / town / city opted for.

h) Audit firms should preferably have qualified Information System Auditor (CISA/DISA) with necessary exposure of system audit. Since all the branches of the Bank are fully computerized, system audit shall form an integral part of audit of the bank.

i) The applicant can opt for any five branches / units in the order of preference either in one or two Centre / Town / City.

j) Audit firm should not have been disqualified by any Bank IBA/RBI/ICAI, while taking-up audit work on earlier occasions.

k) Weightage would be given to the CA firms where the partners themselves are ex-bankers or the firm(s) has got tie-up with ex-bankers with requisite experience and exposure.

I) It is to be ensured that the audit firm or any sister / associate concern / network firm is not conducting the statutory audit of the Bank or any of its branches.

m) Weightage will be given to a firm having exposure in conducting Concurrent Audit of the Bank branches for public sector / major private sector banks.

n) The firm should have necessary office set up and adequate personnel to ensure proper deployment and timely completion of the assignments. The Headquarter or branch of the CA firm should be located at the place for which they wish to take up audit work. Preference would be given to CA firms which are located at the places of our Bank’s Branches.

o) The assignment should be carried out in a professional manner and in case of any misconduct or negligence, The Bank is free to report the matter at any time to ICAI / IBA/RBI. This will be in addition to the disengagement from the Concurrent Audit assignment.

p) The firm will not be allowed to sub-contract the audit work assigned to any outside firm or other persons even though such persons are qualified chartered accountants.

q) A declaration to be furnished by the firm that credit facilities availed by the firm or partners of firm in which they are partners or directors, including any facility availed by a third party for which the firm or its partners are guarantor/s, have not turned non performing asset or are existing non- performing assets, as per the prudential norms of RBI. In case the declaration is found incorrect the assignment would be immediately terminated, besides the firm being liable for any action under ICAI/ RBI/IBA guidelines.

r) The firm should execute undertaking of fidelity and secrecy on its letter head in the format prescribed by the Bank.

s) Concurrent Auditors would have to sign Do’s & Don’ts statement in order to have proper arms length relationship with the Branch/ Department of which they are conducting Concurrent Audit. Such undertaking would be submitted annually.

t) Any other terms and conditions of the assignment as decided by the Bank from time to time.

II. SCOPE OF CONCURRENT AUDIT:

1. Areas covered in the Bank’s Standard format/module for Concurrent Audit specify the scope of Concurrent Audit. Concurrent Auditor would examine all the transactions and identify the ones which are not as per the Bank’s laid down rules/circulars and guidelines/instructions received from regulators & authorities like Govt. of India, RBI & SEBI etc. from time to time.

2. Every quarter Concurrent Auditor would also check if there is any wide variation in the cost of deposits and yield on advances as compared to the previous periods as well as Zonal average figures. A copy of the guidelines on the manner of conducting the audit will be provided to the firm at the time of allotment of branches and thereafter from time to time.

3. Concurrent Auditors will also get rectified all the irregularities identified by them during the course of the audit. Monthly Concurrent Audit reports should be released within 15th of succeeding month and Quarterly Concurrent Audit reports should be submitted within 10ih of succeeding quarter.

4. Comment on Bank’s policies or Evaluation of the decisions taken by Branch Managers/authorized officials are beyond the scope of Concurrent Audit. However, any violation of delegated powers as laid down by the bank and violations of laid down policies, system & procedures of the Bank are within the scope of the Concurrent Audit.

III. REQUIREMENTS FROM AUDIT FIRMS:

1. Bank would provide to the Concurrent Auditors a suggestive/illustrative checklist of items/areas to be checked daily/weekly/monthly/quarterly and Concurrent Auditors should identify the deficiencies/irregularities in accordance with the checklist.

2. Concurrent Auditors shall be required to get rectified all the irregularities identified by them during the course of Audit and report only those irregularities, which remained un-rectified, with reasons as to why the same were not rectified and release the Concurrent Audit Report on or before 15th day of succeeding., month. Branch/offices under manual Audit would submit the Monthly/Quarterly report to respective Branch/Zonal Office/Field Inspectorate.

3. The Concurrent Auditor would also be required to report immediately to the Bank’s higher authorities wherever any serious irregularity or transactions involving malafide, corrupt practices and gross indiscipline or any fraudulent transaction is detected by them.

4. The Monthly Audit Report has to be released on or before 15th day of succeeding month. Branches/Offices under manual Concurrent Audit are required to be submitted in an approved structured format, provided by the Bank within 10th day of succeeding month. The Quarterly reports should be submitted within 10th day of succeeding quarter. Suitable penal provisions would be applicable for delayed submission of audit reports. The firms should strictly adhere to the format/ Online module and the time limit.

5. In case of monthly Concurrent Audits, Auditor has to visit minimum 4-5 days in a week out of which the Chartered Accountant / Partner of the audit firm shall visit the branch for 3 days in a month, preferably during the end of the month. In case B category Branches, Concurrent Auditor has to visit all working days in a month out of which the Chartered Accountant / Partner of the audit firm shall visit the branch for 4 days in a month to the Auditee Branch/ Office in order to reconcile logs generated from SWIFT on daily basis.

IV. TERMS & CONDITIONS:

(a) Engagement:

Applications received from the Chartered Accountant firms in response to the notification, within the given time limit and in the given format fulfilling the prescribed eligibility criteria shall be empanelled by the Bank. The panel shall remain valid for a period of one year i.e. from 01.10.2021 to 30.09.2022 unless otherwise advised in writing.

(b) Engagement of Concurrent Auditors & other conditions

(i) Suitable firms would be identified for each assignment and be approved taking into account their experience and exposure, similar activity carried out for the Bank or other banks, availability of adequate trained resources, location of the audit unit etc. Such approved Concurrent Auditor’s firms would be issued letters of engagement by the Audit & Inspection Department.

(ii) The tenure of the Concurrent Auditor would be initially for one year and would be subject to renewal every year and can be extended maximum up to a period of 3 years overall at Bank’s discretion.

(iii) After completion of specified maximum period of three years, cooling period of one year would be applicable for a firm to become eligible for next engagement. This will be purely at the discretion of the Bank and no rights whatsoever accrue to the firm for such engagement.

(iv)The Concurrent Auditors should adhere to the audit coverage strictly as per the scope as may be decided by the Bank from time to time.

(v) The Concurrent Auditors should not undertake any other activities / assignment on behalf of the branch or unit, other than the activities for which they are engaged, without obtaining the concurrence of the Head Office, Audit & Inspection Department in writing.

(c) Period of Audit/Assignment:

External Audit firms empanelled/selected would be engaged for a period of one year i.e. from 01.10.2021 to 30.09.2022 for the branches/offices identified for monthly/quarterly Concurrent Audit.

(d) Performance Review:

The performance of the engaged firms would be periodically reviewed, at least once a year and if found unsatisfactory, the Bank may remove the name of the Concurrent Audit firm from the panel of the Bank.

(e) De-engagement:

The engaged firms may be de-engaged at the Bank’s sole discretion. If the performance of the Concurrent Auditor is found unsatisfactory or any serious act of omission or commission is noticed in their working, their engagement may be cancelled at any point of time. If felt necessary, the matter may be reported to ICAI and/or RBI/IBA for necessary action.

1. If any of the information / documents furnished by the auditor is found to be untrue / incorrect, the Bank’s offer shall automatically stand cancelled without entertaining any further correspondence.

2. Deliberate omission of facts, information about disqualification which comes to the knowledge of bank at a later date will lead to premature termination.

3. Any serious acts of Commissions, omissions, misconduct, deviations in professional ethics or any other reason bank may deem fit and appropriate to the situation.

4. Reported disqualification as per Section 141 of Companies Act 2013 for appointment as auditors of the Bank and also as given in Section 141 of the Companies Act read with Rule 10 of The Companies (Audit and Auditors) Rules, 2014.

5. In case the application is rejected for reasons mentioned above, the Bank shall identify a new auditor for the branch, at its discretion and the applicant shall not claim any right for audit of said or any other branch.

6. Bank reserves the right to terminate & de-panel the empanelment forthwith without any notice and without assigning any reasons in case of (i) proven misconduct (ii) getting any adverse reports or adverse confidential information (iii) bank feels that its interests may be jeopardized besides reserving its rights for initiating other action as deemed fit.

7. The empaneled ECAs may request for relinquishment of audit assignment due to reasons like death of partner, health grounds; availing of credit facilities from our bank either by the auditor or his relatives.

8. The appointment for Concurrent Audit is purely contractual and for a specific period of 12 months and the same may be renewed on a yearly basis (twice) subject to satisfactory performance / eligibility of the particular branch for Concurrent Audit. The maximum period of contract shall be restricted to 36 months. However, the Bank reserves the right to terminate the contract at any point of time for whatsoever reasons as the Bank may deem fit.

9. Whenever, the assignment is terminated or relinquishment is permitted, the External Concurrent Auditors concerned are eligible for audit remuneration only up to the end of previous month for which a fully completed report is received. In such cases, Bank reserves the right (i) to adjust the same (audit remuneration) towards commission / omission if any or (ii) withhold the same for a period of 6 months or till suitable administrative decision is taken whichever is earlier

10. After termination of the contract, the auditor / firm shall not use or keep any of the material information given by the Bank like Manuals, circulars etc. or make any representations to public or outsiders as continuing this contract. The auditor / firm shall return all materials belonging to the Bank after termination of this contract / agreement, unless otherwise instructed in writing by the Bank.

11. Whenever termination is made, the ECA shall have no right to demand fees for the unexpired period of empanelment/contract on any ground whatsoever

12. The Bank shall have the absolute discretion in allotting the branch, revising fee structure, stipulating terms and conditions of the appointment like experience in Concurrent Audit of our branches / other banks etc. and termination of the services of the empaneled auditor after giving due notice at any point of time including during the pendency of the contract.

13. Due to rationalization of branches, if any Branch/ Unit merges with another Branch/Unit you will be given opportunity to conduct Concurrent Audit of the acquired Branch subject to the acquiring Branch/ Unit is not under External Concurrent Audit. If the acquiring Branch is already under Concurrent Audit by External Chartered Accountant, then your firm shall forgo the assignment. In this regard, decision of Audit & Inspection Department, Head office will be final.

(f) Application processes:

Application is to be made Online. Auditors have to submit a preference of five branches from the enclosed list of branches identified for audit during the year 01.10.2021 to 30.09.2022.

The online application portal will remain open from 13.09.2021 to 18.09.2021 (23:59:59 Firs)

Please note that while filling up online application, the system will display the APPLICATION ID and PASS WORD at the top of second page of online application i.e. after clicking SAVE & NEXT button of first page. Please note the same immediately for your future reference.

After Final SUBMISSION of the application, the system will not allow to edit or modify ‘ your application. Please take the print of your submitted application immediately after clicking FINAL SUBMISSION for your future reference and record.

No need to send the application by post /mail.

(g) Documents to be submitted with the application:

No documents need to be submitted with online application. But in the event of any Firm being selected for engagement as Concurrent Auditor of any of our branches, they are required to furnish printed copy of online application duly signed by the authorised person, self attested photocopies of all documents along with Original documents in support of their credentials furnished in application to their respective Field inspectorate for verification and record. The original will be returned after verification.

In case any of the information furnished by the Firm in application found to be inconsistent with Original documents, the selection of the Firm will be cancelled forthwith. Further, if any such inconsistency (ies) noticed subsequent to engagement even post verification of documents, the engagement will be discontinued with appropriate reporting of Firms name to RBI/IBA/ICAI etc.

The Bank shall send engagement letters to all selected Chartered Accountant firms through respective Field inspectorates having jurisdiction over the concerned branches. However, CA firms which do not get our letter of engagement are to be treated as ” NOT SELECTED” and no further correspondence shall be entertained in respect of fate of their application.

THE BANK RESERVES THE RIGHT TO ACCEPT OR REJECT ANY APPLICATION AT ANY TIME WITHOUT ANY LIABILITY AND ASSIGNING ANY REASONS THEREOF.

(h) Evaluation of applications;

The application received by the bank would be screened by a Committee of Executives constituted for this purpose, which will consider engagement of CA firms on a scoring system based on their experience, CISA /DISA qualifications number of partners, seniority, CA firms having tie-up with Ex-Bankers etc. and any other factor considered necessary by the committee for which the decision of the Committee shall be final.

Merely meeting the eligibility criteria shall not automatically entitle the firm for engagement. After engagement, the work will be allotted as and when need arises at the sole discreation of the Bank. The engagement will not give any right to the empanelled firms for carrying out the assignment. The Bank reserves its right to cancel any or all the offers without assigning any reason whatsoever.

(I) Selection of Concurrent Auditors:

Selection of Concurrent Auditors shall be made from among the applications received from the Chartered Accountant firms by the Audit & Inspection department on the basis of a scoring system. The approval of the selected Concurrent Auditors would be done by a committee consisting of three executives. The list of selected Concurrent Auditors would be placed before the top management of the Bank for final approval.

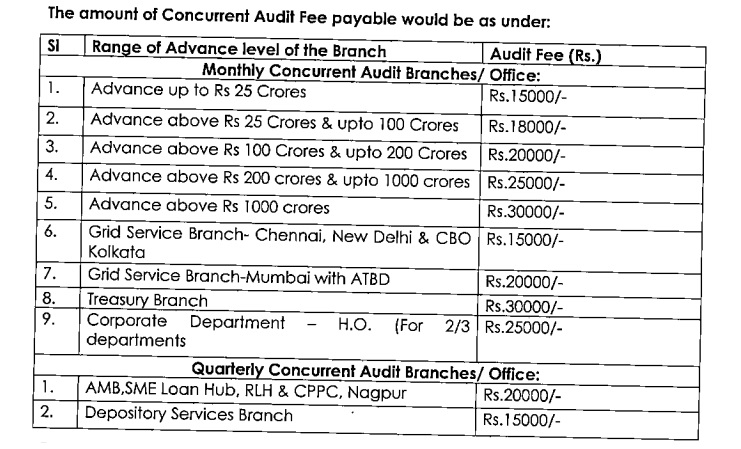

V. Payment Terms:

The audit fee shall be paid to the firm as decided by the Bank from time to time and mentioned in offer letter for allotment of assignment, on submission of the relevant audit reports and the relevant bill along with supporting documents. The following schedule of fees being paid by the Bank depending on the volume of advances at the branch.

In the case of any changes of advance figure during current audit year i.e. 2021-22, the fees will remain same for that year.

No out of pocket expenses or traveling allowance/ halting allowance would be paid to the Concurrent Auditors. However, Goods & Service Tax etc. would be paid as applicable in addition to the Audit Fees. The payment to Concurrent Auditors would be subject to TDS at the applicable rates.

The amount of Concurrent Audit Fee payable would be as under: